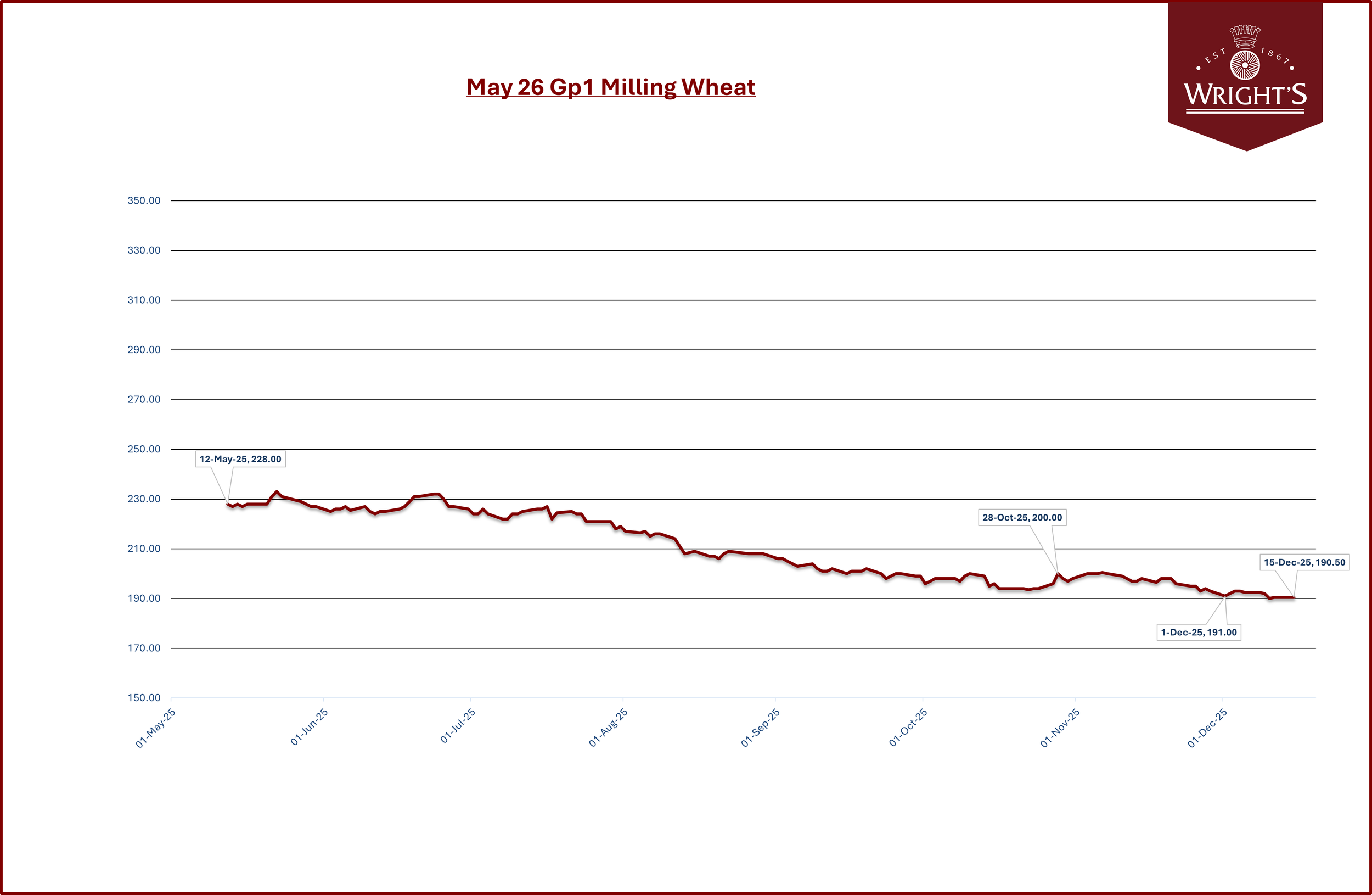

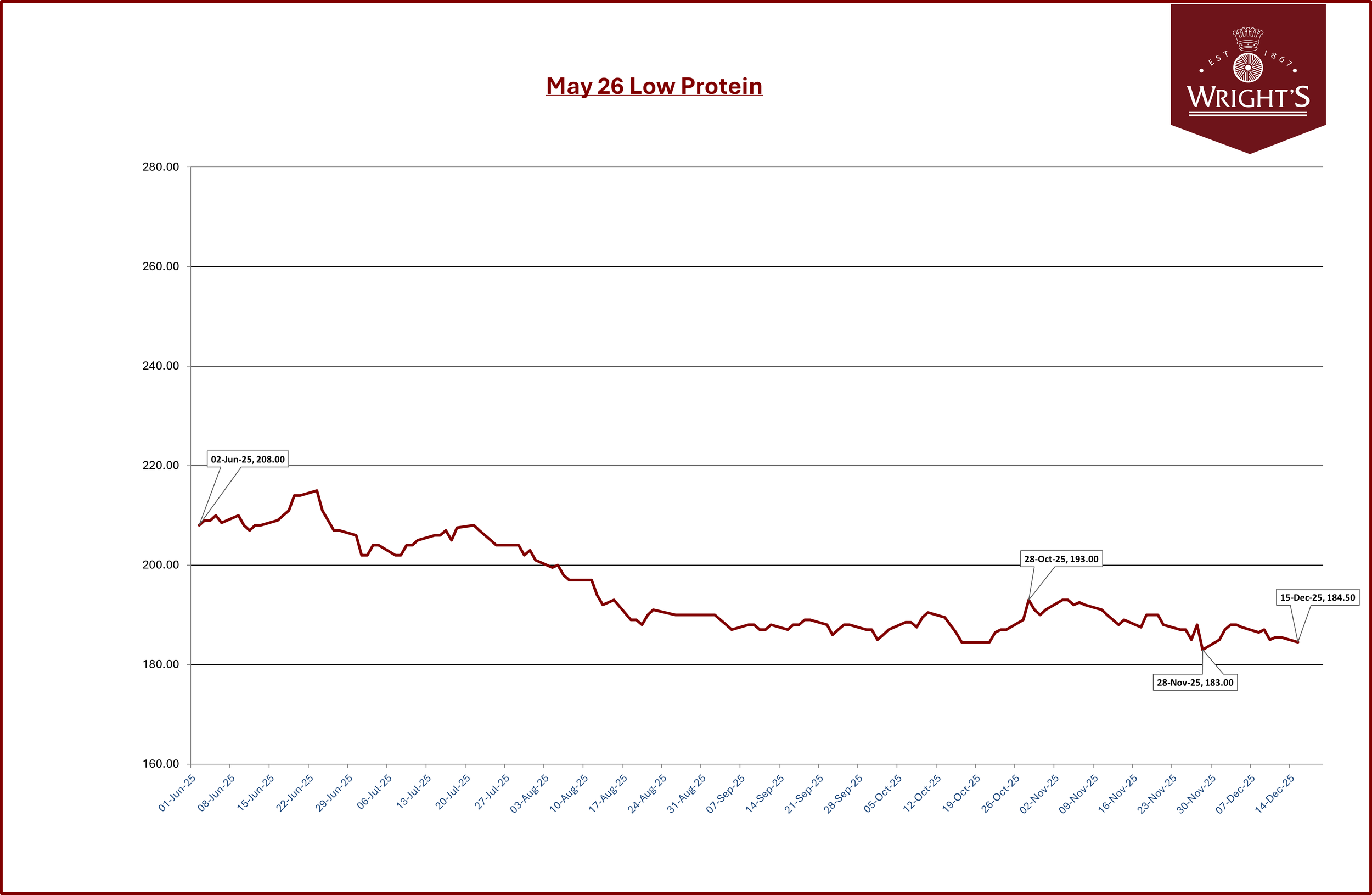

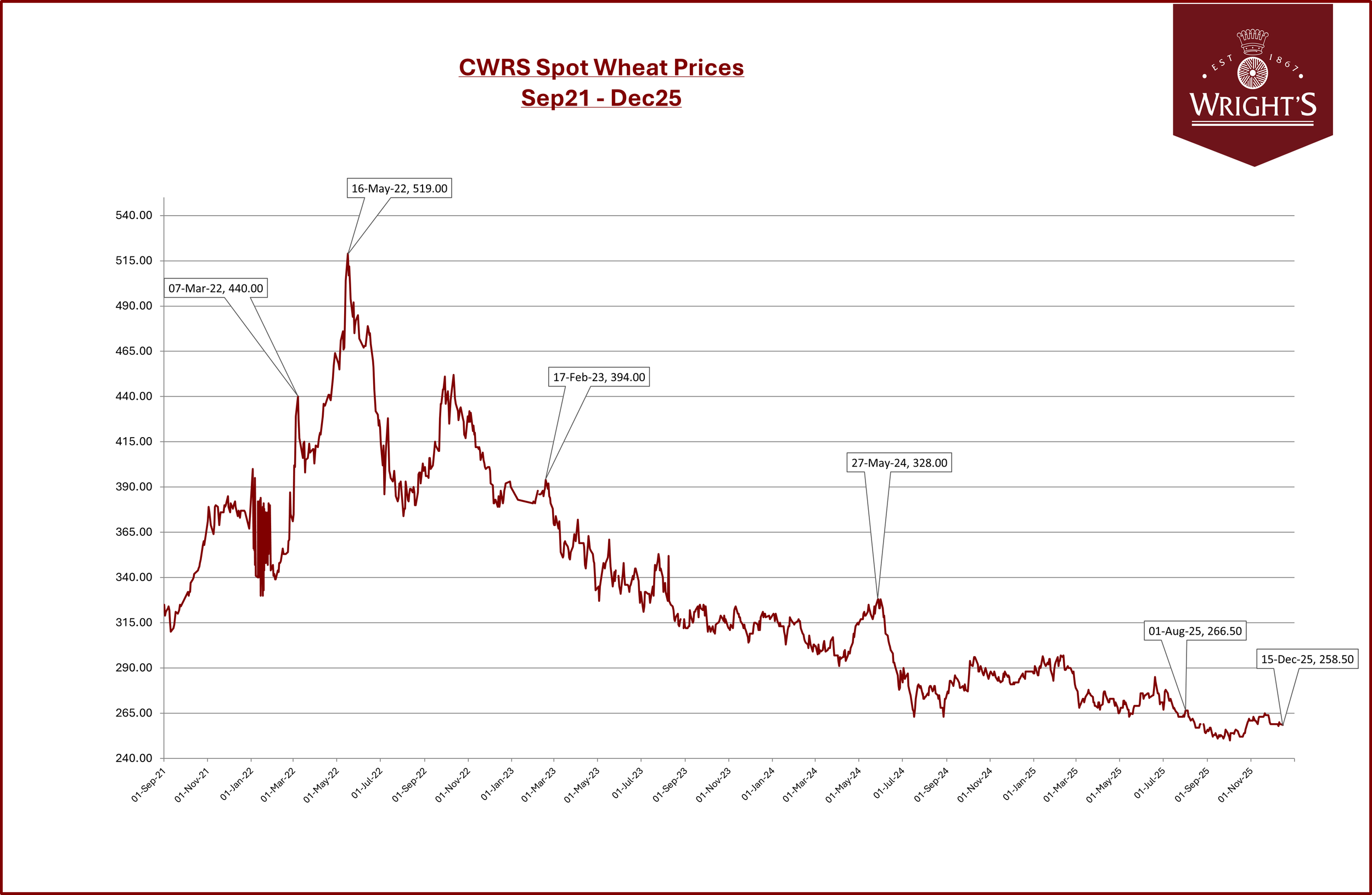

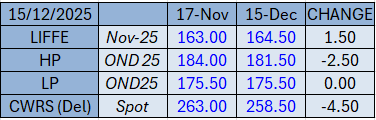

Wheat Market Update - 15th December 2025

I. Executive Summary

The overall trend for both global and UK wheat prices over the past month has been downward / sideways, continuing a period of pressure.

The key factors driving this bearish (downward) sentiment are:

Ample Global Supply: The USDA's December WASDE (World Agricultural Supply and Demand Estimates) report increased forecasts for global production and ending stocks for the 2025/26 season, reflecting high output in key exporters.

Black Sea and South American Competition: Aggressive, competitively priced exports from Russia and rising production/exports from the Southern Hemisphere (Argentina and Australia) are dominating international trade flows.

Limited Geopolitical Premium: Despite ongoing conflict in the Black Sea region, the market is largely ignoring geopolitical risk unless there is a material disruption to export logistics, limiting the 'war premium' on prices.

II. UK Market Focus

LIFFE UK wheat prices have remained under significant pressure, closely following the negative global trend.

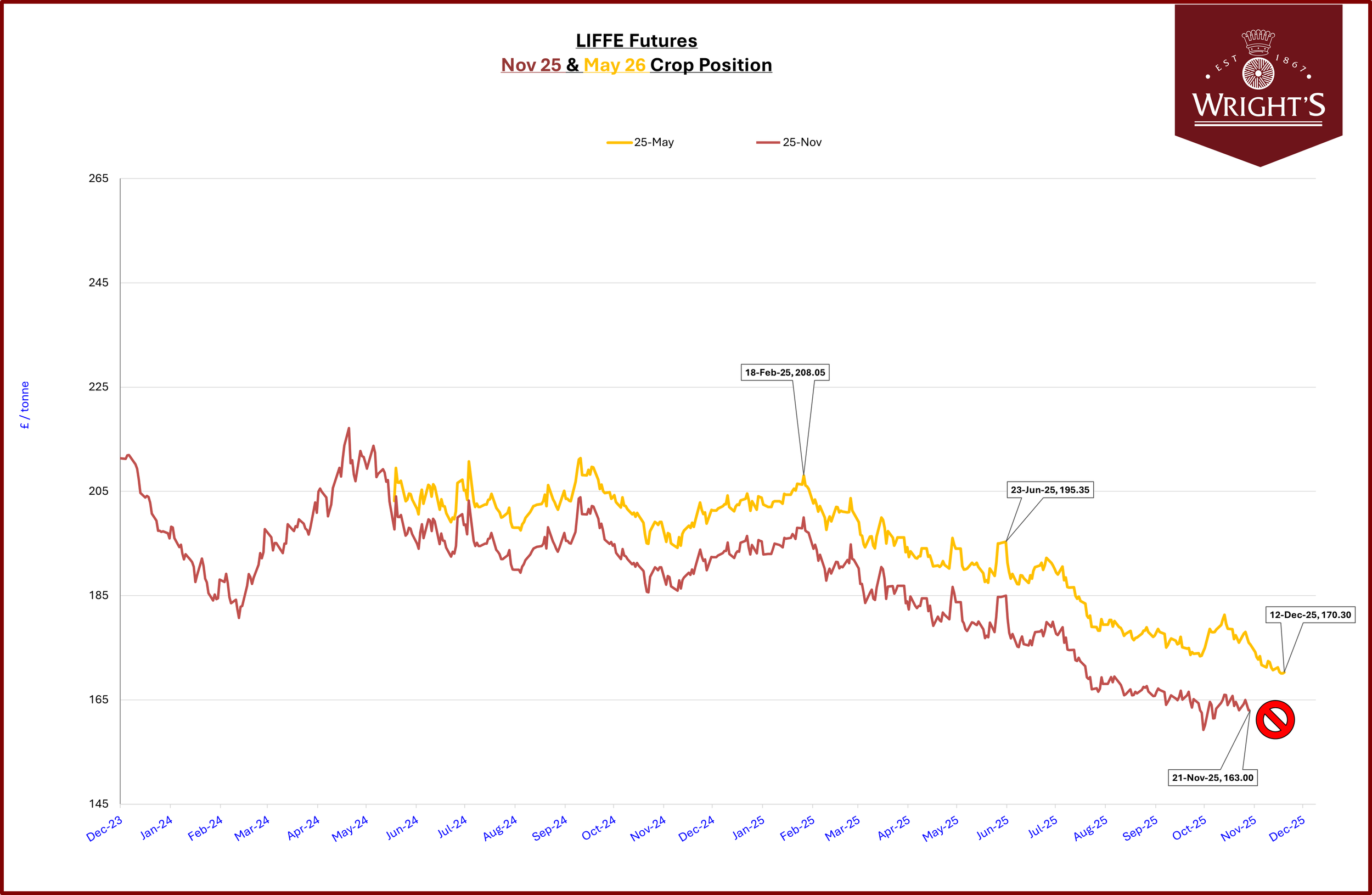

LIFFE Futures Levels: The nearby May-26 contract has seen a decrease over the month, with prices settling near £170 - £172 at mid-December, nearing a new contract low of £170.35, which was recently recorded

Currency Movements: The pound sterling ($\text{GBP}$) has fluctuated. A weaker sterling against the US Dollar ($\text{USD}$) occasionally provides a marginal shelter for domestic prices by making UK exports more competitive and imports more expensive. Conversely, a stronger sterling weighs on domestic futures.

Domestic Crop Outlook and Trade:

UK domestic production estimates for the 2025 harvest are up by approximately 7.3% to 11.96 million tonnes, driven by an expansion in planted area. This comfortable domestic supply adds internal downward pressure.

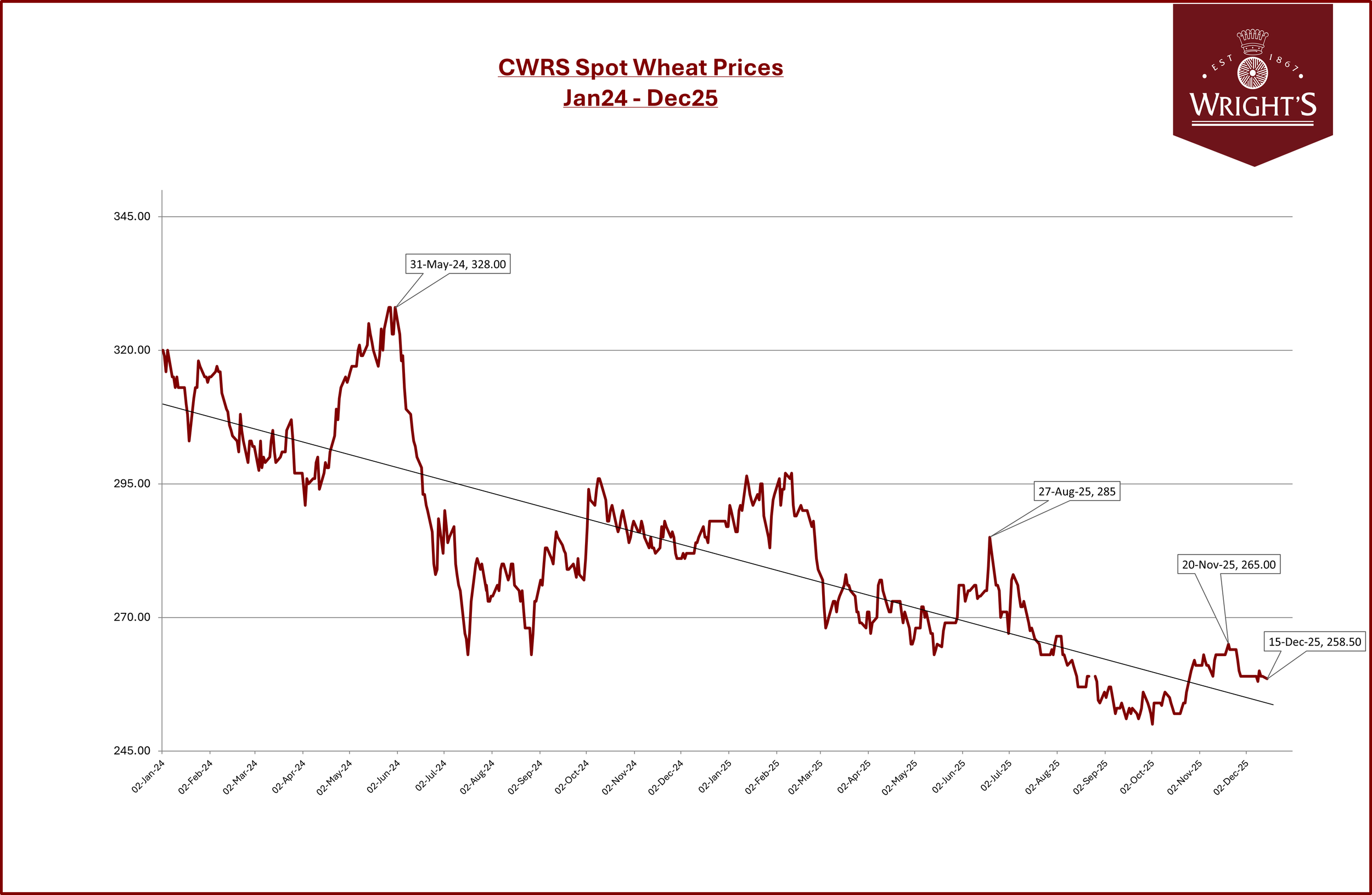

Competition from cheaper EU wheat, pressured by a strong Euro ($\text{EUR}$) and Black Sea exports, is limiting the UK's export opportunities, especially into Continental Europe.

III. Global Wheat Outlook

International price benchmarks have trended lower, reinforcing the global narrative of surplus supply.

USDA/IGC Updates: The December USDA WASDE report was bearish, raising the global wheat production forecast to 837.8 million tonnes and increasing global ending stocks to 274.9 million tonnes (the highest since 2021/22).

Major Exporters:

Russia: Continues to exert strong downward pressure with a large harvest and aggressively competitive export offers.

EU: Production has rebounded, leading to a high exportable supply, which a strong Euro is making harder to move competitively on the global market.

Australia & Argentina: Both are expected to have historically large harvests, adding significant new-crop supply to global trade flows, particularly into Asian and North African markets.

Logistical Factors: Argentina's announcement of cuts to export taxes on wheat and other grains is expected to boost its export competitiveness further and increase global flows.

IV. Outlook for the Next Month

The immediate outlook remains bearish/steady. Fundamentals are heavily tilted towards oversupply, especially following the December WASDE report.

Any significant upward price movement in the next month is likely to be technical (short-covering by funds) or dependent on a new, material supply disruption from unexpected severe Black Sea weather (cold snap/drought concerns) or a major geopolitical escalation that directly impacts key shipping lanes. Barring these events, prices are expected to continue probing recent lows as Northern Hemisphere exporters compete fiercely against fresh Southern Hemisphere supplies.