Wheat Market Update - 10th February 2026

I. Executive Summary

The near-term picture is one of relatively stable pricing with limited downside given the tight domestic balance, but equally limited upside given the global surplus. The compressed milling premium presents a buying opportunity for those not yet covered, though it is unlikely to narrow much further from current levels. The key watchpoints are: weather developments in Russia and Ukraine through February and March; sterling’s trajectory against the dollar and euro; and todays WASDE for any adjustments to the global stocks picture. For new crop (2026 harvest), AHDB reports 83% of UK winter wheat in good or excellent condition – the best start since the 2023 crop – which, if sustained, could deliver a UK crop above 13 MMT and ease the current tight supply position into next season.

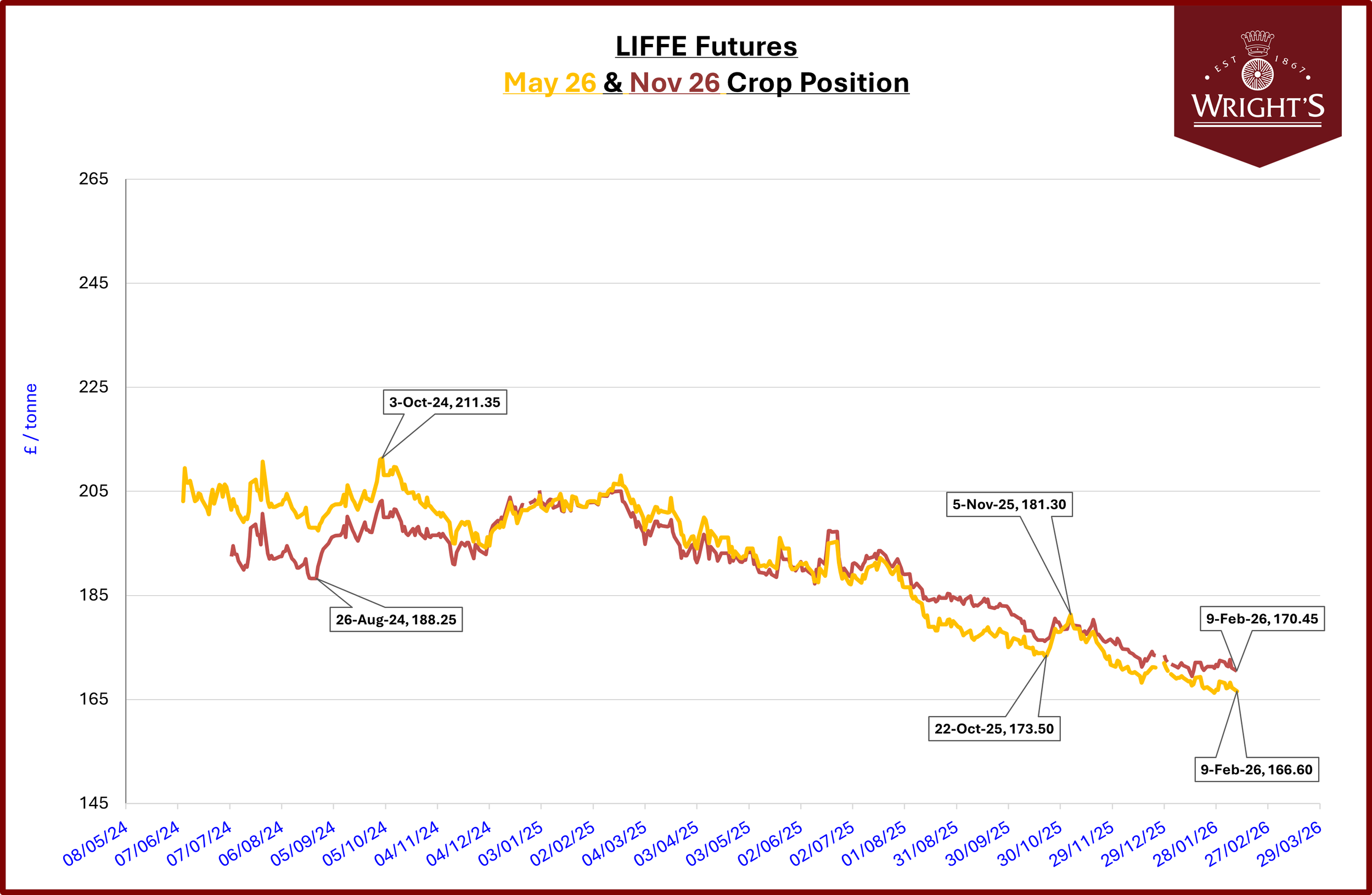

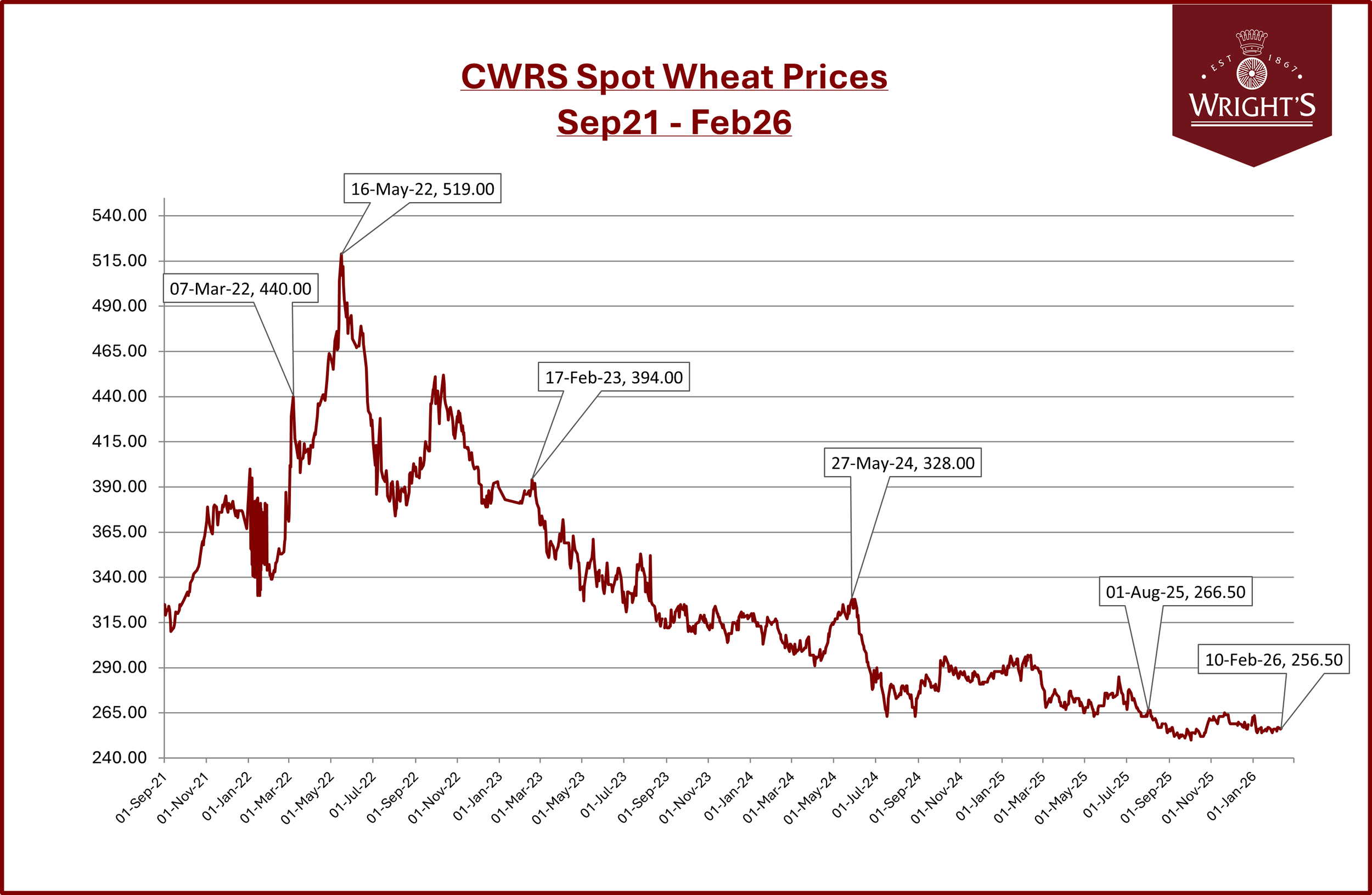

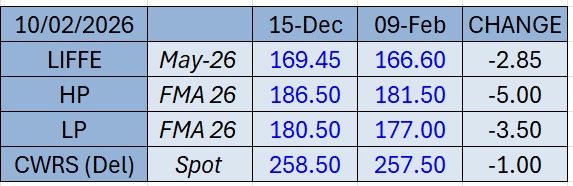

Price Movement: UK LIFFE feed wheat (May-26) closed at £166.26/t a modest decrease from prices seen in December 25 from our last update. This is a modest £2.85 downward movement

Supply Outlook: Global wheat ending stocks for 2025/26 are projected at 278.3 MMT, the highest in five years. The picture remains one of oversupply.

Market Consolidation: Market commentators suggest we may now be in a period of consolidation, with wheat prices in many key producing regions at or below the cost of production. Historically, this has led to reduced planted areas, tighter supply, and ultimately upward pressure on prices.

II. UK Market Focus

The UK market is currently navigating a "tighter but quieter" balance sheet. Although domestic production for the 2025/26 season was lower than in previous years, a significant drop in industrial demand—specifically from the bioethanol and distilling sectors—has mitigated supply concerns.

Futures & Delivered Prices: London LIFFE May-26 futures are consolidating around the £166.26/t support level. Prices continue to see a general sideways, slight downwards movement.

Import Dynamics: Wheat imports for the 2025/26 season are pegged at 2.20 MMT, down 28% from the record levels seen last year.

Currency Impact: The strength of the Sterling (£1 = $1.38 in late January) has been a double-edged sword; it has kept a lid on domestic price rallies but made UK exports uncompetitive.

III. Global Wheat Outlook

The global wheat complex is currently caught between bearish supply fundamentals and emerging weather-related risks. While the market is fundamentally oversupplied, recent support has come from concerns regarding winterkill in Ukraine and parts of the US Plains, where low snow cover has left crops vulnerable to deep frosts.

Black Sea Dynamics: Russia continues to dominate the export market, with SovEcon raising its 2025/26 export forecast by 1.1 MMT to 45.7 MMT. Despite ongoing conflict, Russian wheat prices rose for a third consecutive week, driven primarily by internal logistical bottlenecks rather than a shortage of grain.

EU Production: The COCERAL December forecast projects 2026 EU soft wheat production at 129.7 MMT, a 4% decrease from 2025’s exceptional yields. However, current EU ending stocks have been revised upward by 1.3 MMT to 13.0 MMT due to intense competition from lower-cost Black Sea origins, which has reduced EU exports.