Wheat Market Update - 15th September 2025

I. Executive Summary

A relatively unexciting month has seen the wheat market continue to decline. A combination of a robust UK harvest (specifically Winter Wheats), a lack of consumer demand, and ample global supply from key producers has kept prices subdued. The UK harvest is complete, with UK Group 1 Milling wheat qualities looking good, with good protein levels and specific weights.

II. UK Market Focus

The UK harvest is now completed, and while yields have shown significant variability, overall progress has been ahead of the usual pace. The good news is that despite the mixed results, the quality of the wheat harvested so far, particularly in terms of protein and specific weight, has been promising.

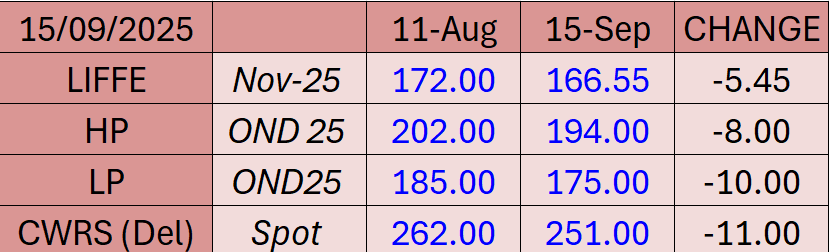

London wheat futures closed on Friday with the November 25 contract at £166.25 and the November 26 contract at £183.00

A reluctance to sell among farmers (due to low prices) and a continued downward/sideways movement in futures prices have meant that physical wheat prices have remained under pressure. The overall abundance of domestic supply, coupled with record-high imports from the last marketing year, has maintained a bearish sentiment in the market.

The AHDB has updated its UK wheat average yield to 7.6t ha (compared to 7.3t ha last year and a 10-year average of 8.1t ha), while Argus (previously Strategie Grains) estimates the yield to be 7.39t ha. It is also challenging to assess consumption requirements, given the slow demand from various sectors of the UK food industry. The UK market continues to trade at, or close to, import parity.

III. Global Wheat Outlook

The latest USDA WASDE report, released last week, reinforced the bearish global outlook. The report raised its forecast for global wheat production by a total of 9.3 million metric tons for the 2025/26 season, driven by a particularly large crop in Russia, where the estimate was increased to 85.0 million metric tons. While the US is seeing a strong pace of exports, particularly for hard red winter wheat, with exports raised by 25 million bushels to 900 million, this is being offset by aggressive competition from other countries.

A revised, larger US corn crop (427.11 million tonnes) with an increase in the planted area was reported, more than offsetting a small reduction in their yield estimate. The USDA holds UK wheat production unchanged at 12.5 mmt. Many trade estimates are lower than this.

The market continues to be dominated by a significant supply surplus, which is the main factor preventing prices from recovering. The abundant international supply, combined with geopolitical tensions that are not significantly disrupting trade, means market sentiment remains focused on the downside.