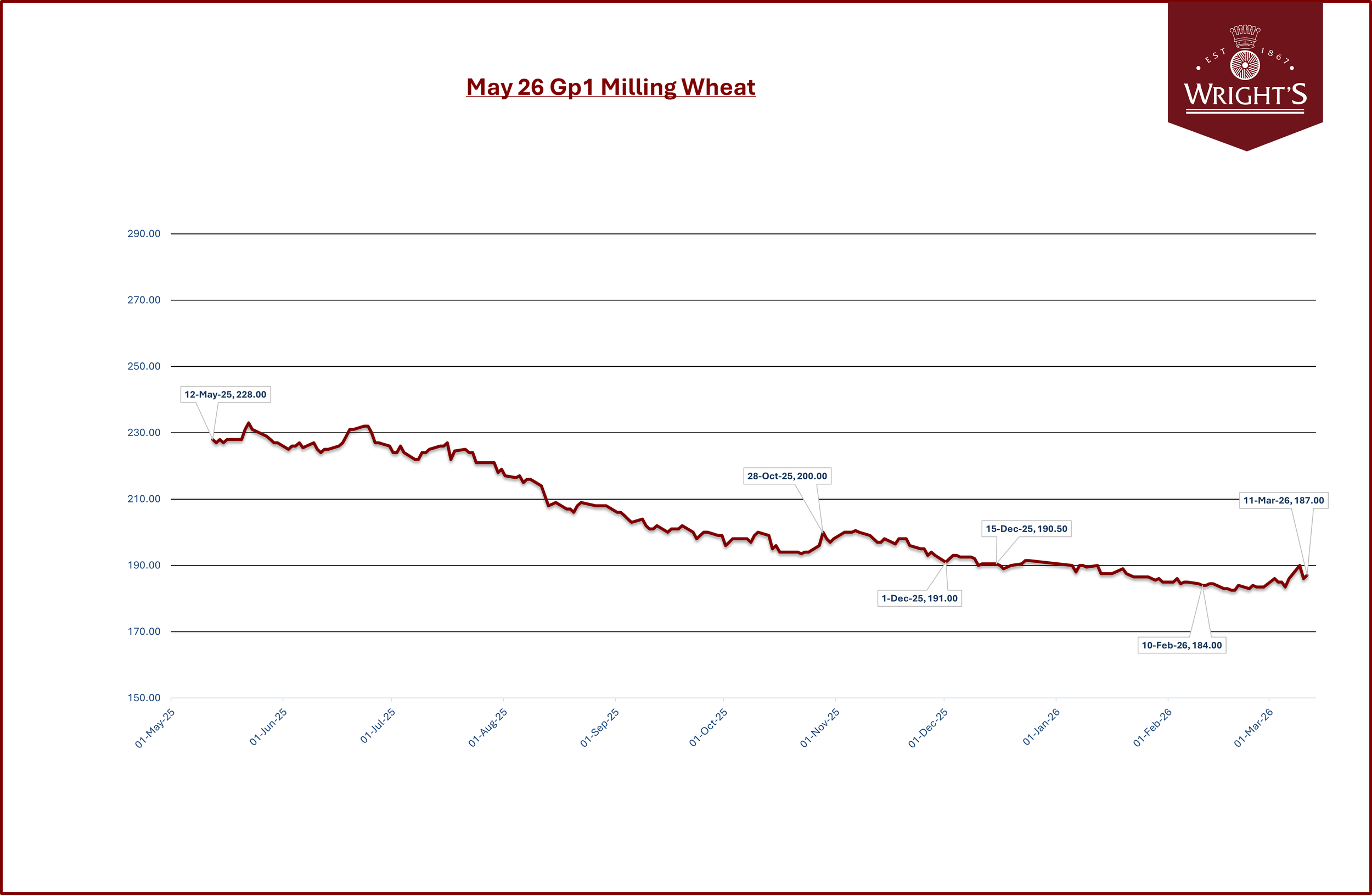

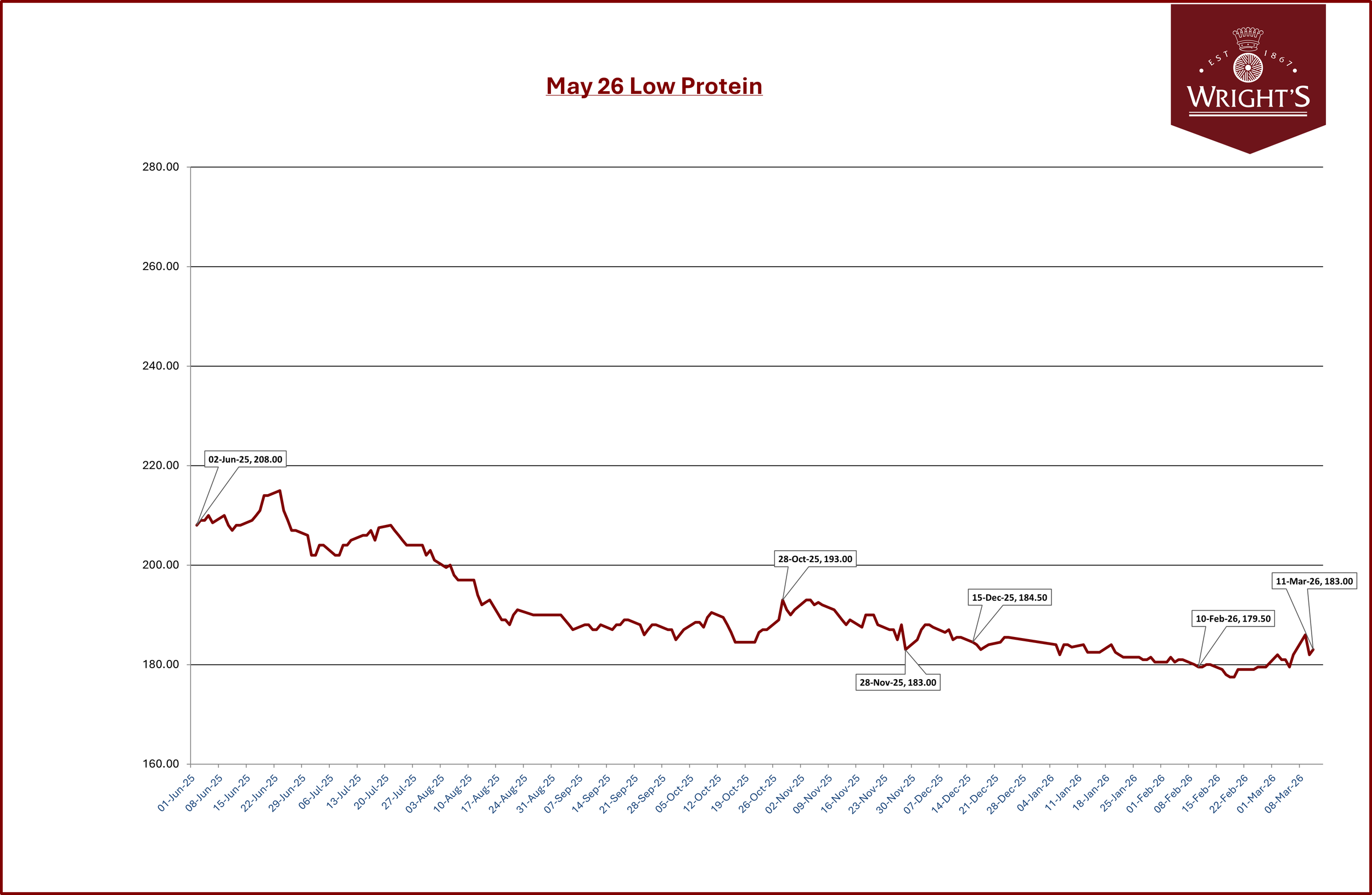

Wheat Market Update - 11th March 2026

Executive Summary

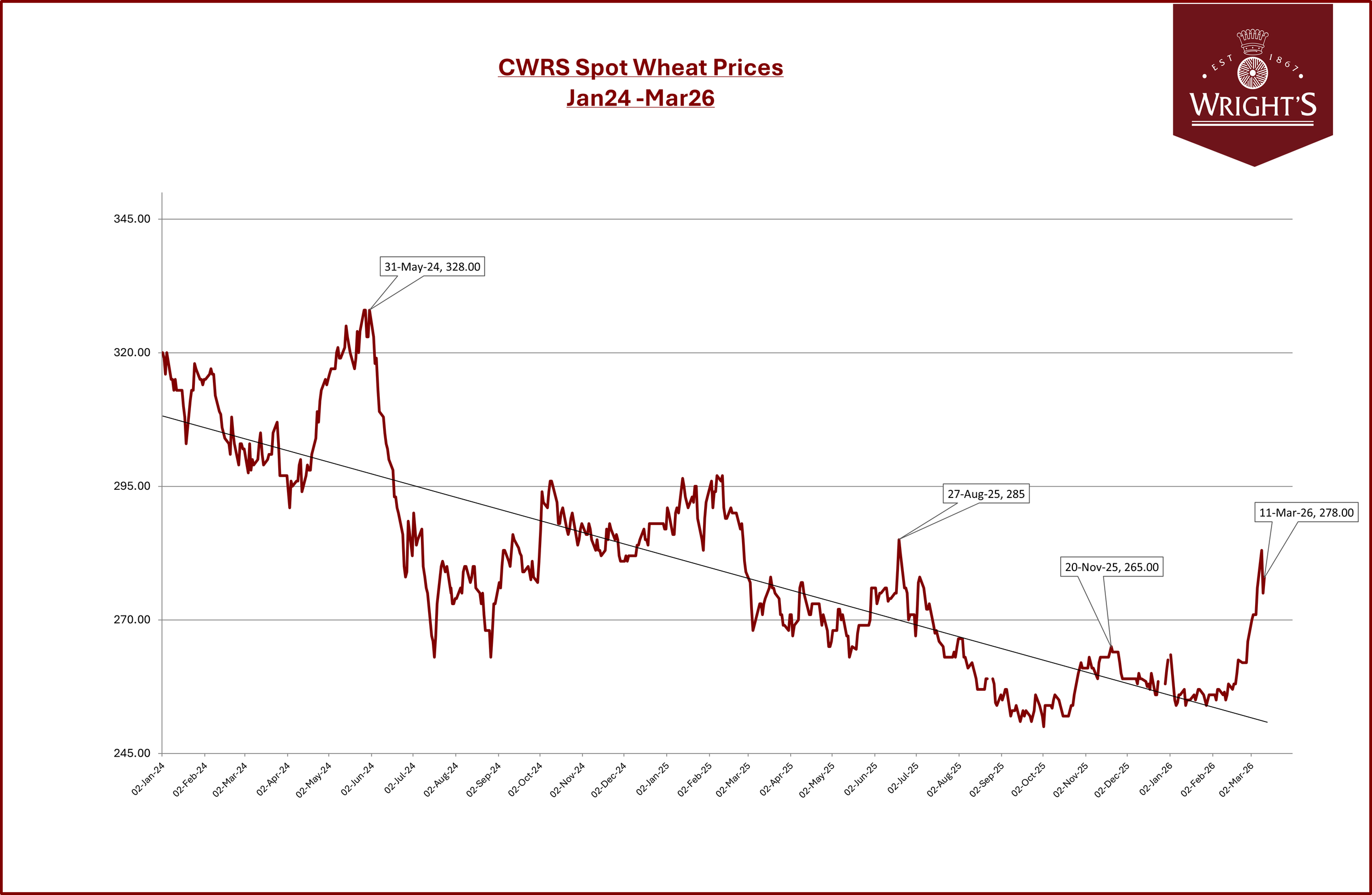

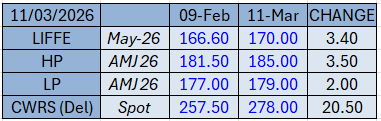

Global and UK wheat prices have moved higher since the start of the month. After trading sideways through much of February, markets surged in early March, with Chicago (CBOT) May wheat breaking back above $6.00/bushel for the first time since February 2025. UK feed wheat futures (May-26) rose from around £167/t in mid-February to approximately £175/t by early March, with levels touching the highest since November 2025.

The key drivers behind the move are:

Geopolitical risk premium: An escalation of conflict in the Middle East, involving Iran and its closure of the Strait of Hormuz, has pushed crude oil prices up as high as $113/barrel (this has since dropped back to $85.28). This has fed directly into agricultural commodity markets through rising energy, shipping, and fertiliser costs.

Fund short-covering: Speculative funds held historically large short positions in wheat entering 2026. As prices began to rally, funds covered rapidly — an estimated 31,000 contracts were bought in Chicago in just two days — amplifying the upward move.

Crop condition concerns: Winter wheat ratings in the US Plains remain below average, and forecasts of dry weather for mid-March are raising doubts about spring crop recovery. Northern EU conditions, particularly in Germany, are also being monitored.

Overall, the trend has shifted from broadly bearish to cautiously bullish in the space of a few weeks, though underlying global supply remains ample

UK Market

Futures & Delivered Prices

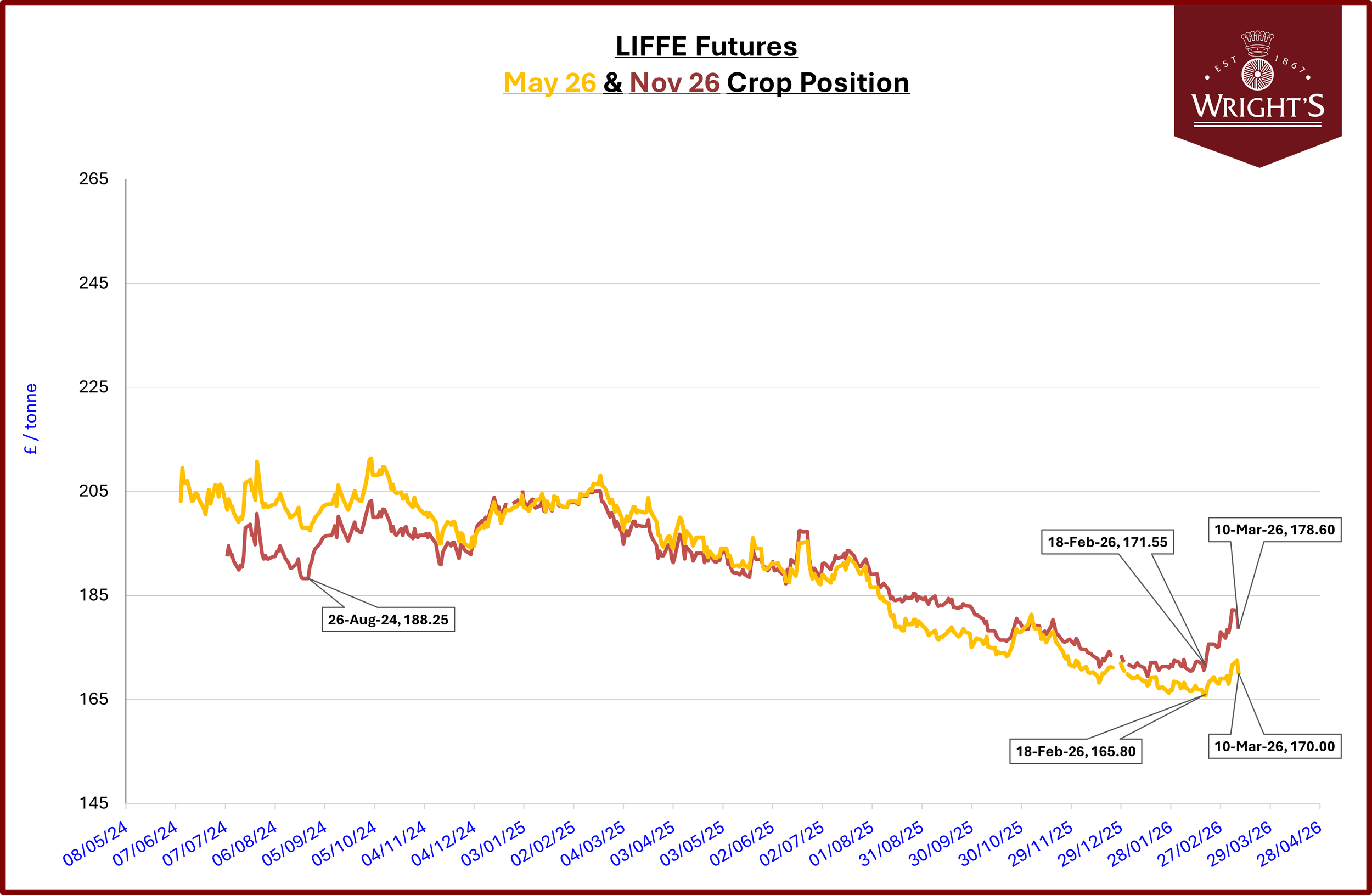

UK feed wheat futures (May-26 contract on ICE) closed at £171.60/t on 6 March, a gain of £2.60/t week-on-week and the highest closing level of 2026. By early trading on 9 March, the contract had risen further to £174.95/t on the back of the crude oil surge. The Nov-26 contract (new crop) touched £185/t, its highest since August 2025.

Domestic Demand & Supply

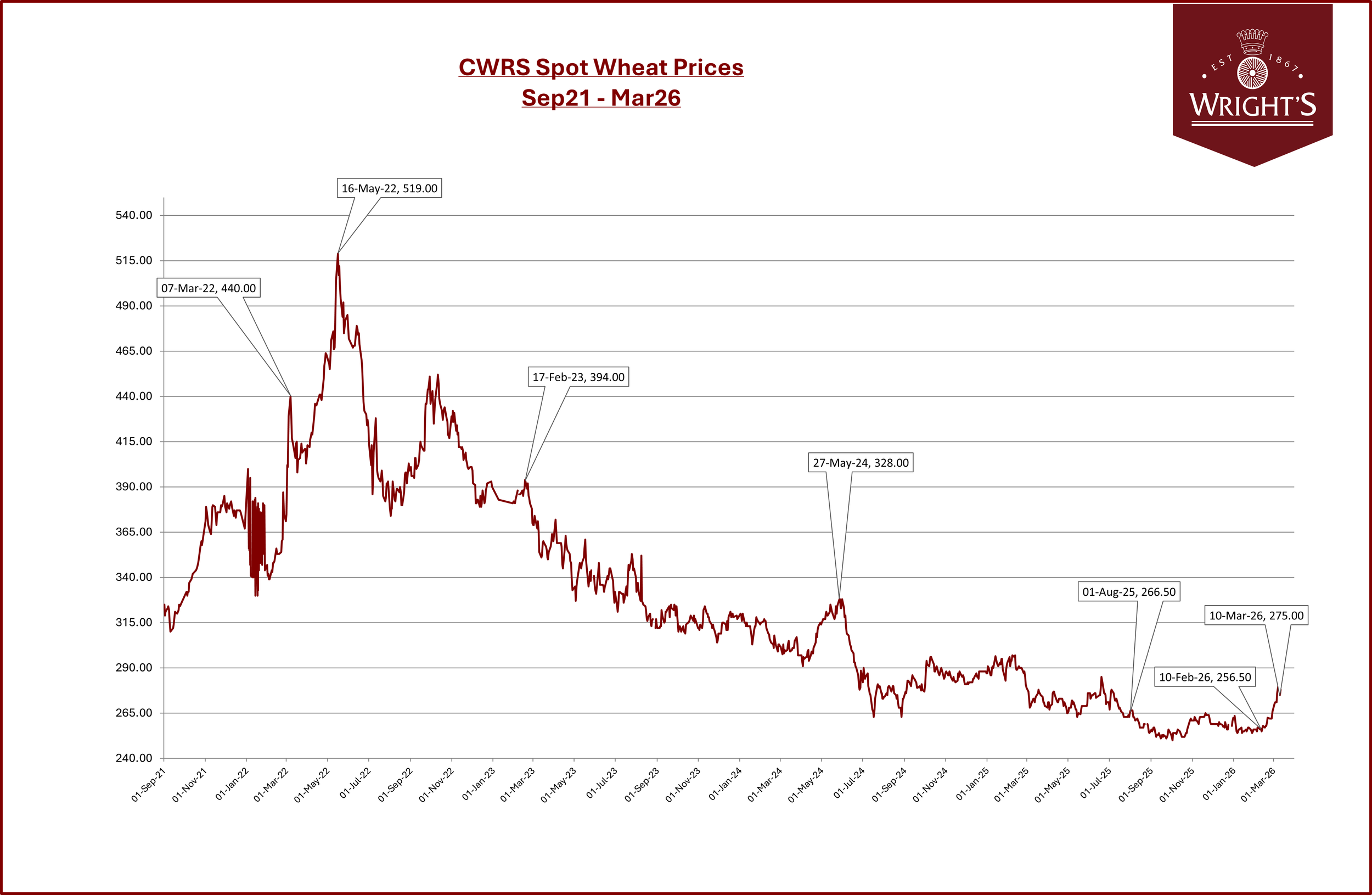

AHDB data shows home-grown wheat milled from July to January (including for bioethanol) fell 2.4% year-on-year, while imported wheat volumes milled dropped 30%. UK wheat imports from July to December 2025 were down 23% on the same period in 2024 at 1.30 Mt. The domestic market has been described as quiet, with limited physical trading activity through February

Global Market

The escalation of conflict involving Iran and threats to shipping through the Strait of Hormuz have driven crude oil above $113/barrel and pushed fertiliser prices to their highest since 2022. Rising energy and input costs are pressuring farm margins globally and increasing production costs across the food supply chain. The US administration continues to signal potential tariff increases from 10% toward 15%, adding further uncertainty to global trade flows.

Implications of the Iran Conflict on the Grain Market

What Happened

On 28 February, US-Israeli strikes on Iran triggered retaliation across the Gulf. Iran has effectively closed the Strait of Hormuz — through which 21% of global oil supply and 20–30% of global fertiliser exports transit. Shipping through the Strait has dropped by over 70%. At least ten commercial vessels have been attacked, and major carriers are rerouting via the Cape of Good Hope.

How This Affects Grain Markets

Energy costs: Crude oil has surged 55% in two weeks. Higher diesel prices increase farm, transport and processing costs across the supply chain. UK pump prices are already rising.

Fertiliser shock: Gulf states produce ~15 Mt/year of nitrogen fertiliser. Urea has jumped 33% to above $600/t. With northern hemisphere planting imminent, disruption at this point in the season is difficult to work around. US analysts estimate 1–1.5 million corn acres could shift to soybeans as nitrogen costs rise.

Food security concerns: Iran has banned food exports. Gulf states face disrupted import routes.

Key Difference from Russia-Ukraine (2022)

Iran is a wheat consumer, not an exporter. Unlike 2022, no major wheat-producing nation is directly affected and global stocks remain high (US ending stocks at a seven-year high). The rally is driven by energy costs, fertiliser disruption and speculative flows — not a physical supply shortage. This means prices are more vulnerable to reversal if the conflict de-escalates.

Outlook — Next 30 Days

The near-term outlook is finely balanced between supportive and bearish factors:

Supportive: Geopolitical risk premium in energy markets; rising input costs; dry weather concerns in US Plains and parts of northern Europe; continued fund buying momentum.

Bearish: Global wheat stocks remain high by historical standards; EU and Russian crop conditions are looking good; the rally has been driven more by macro events than by fundamental wheat supply tightness; a de-escalation in the Middle East could quickly reverse the risk premium.

Central expectation: Prices are likely to remain elevated and volatile in the short term, with UK feed wheat (May-26) trading in a range of £170–£180/t. A sustained move higher would require either a deterioration in Northern Hemisphere crop conditions or a further escalation in the Middle East. Conversely, any ceasefire or easing of energy prices could see a sharp pullback.