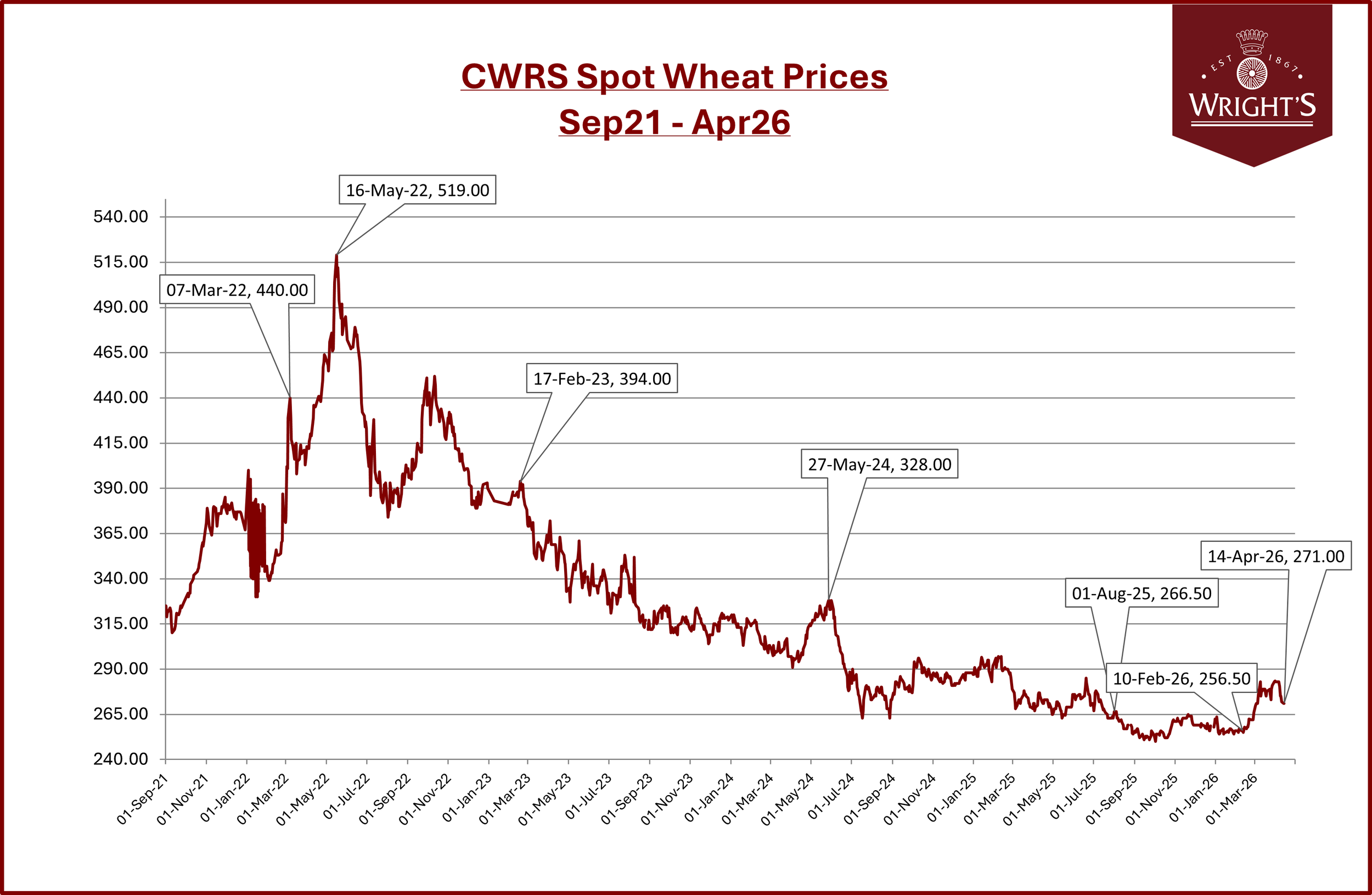

Wheat Market Update - 14th April 2026

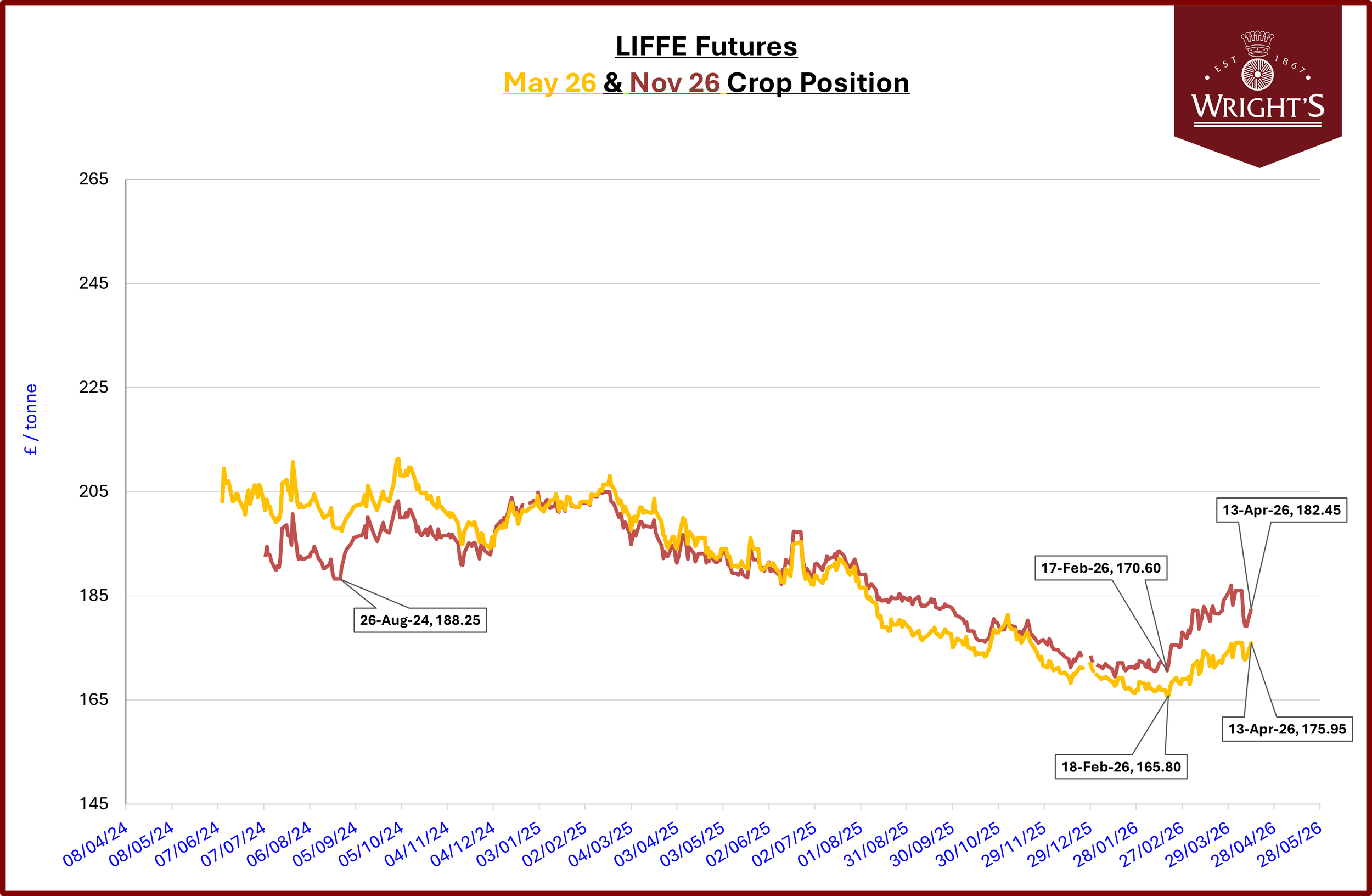

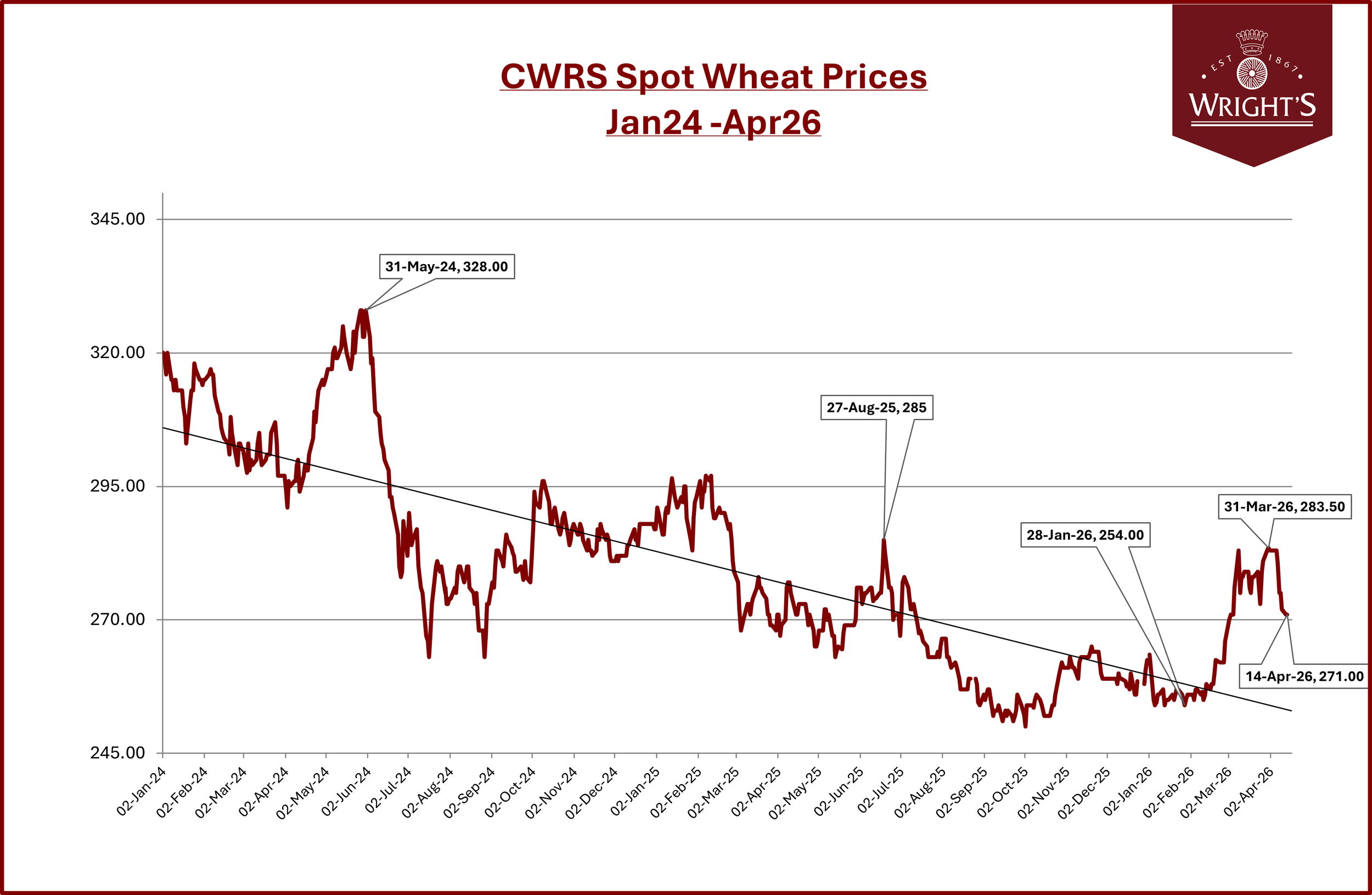

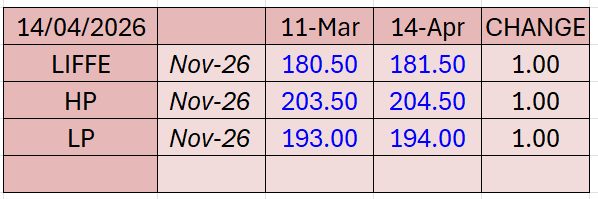

Prices based on Nov-26 Futures

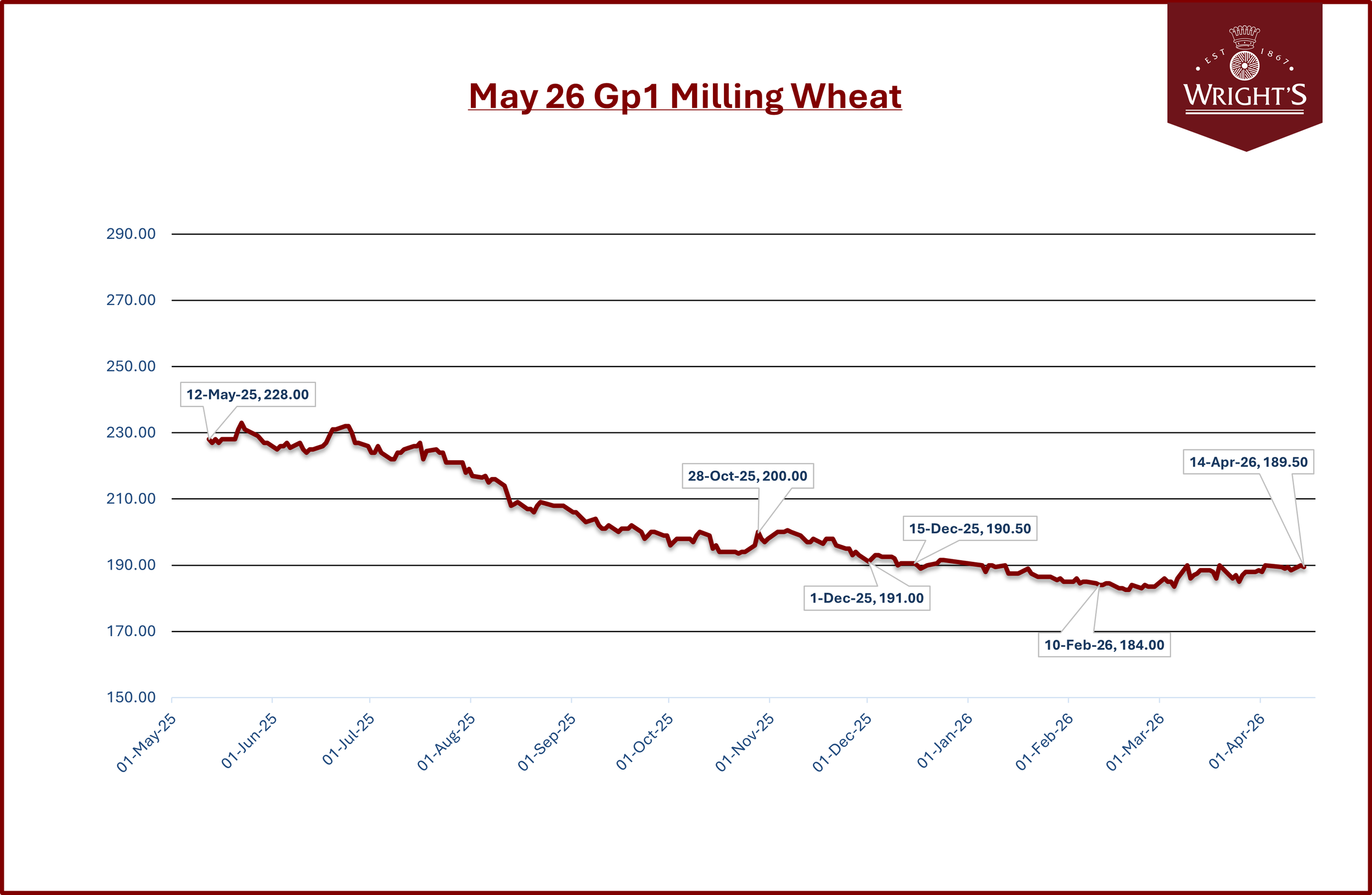

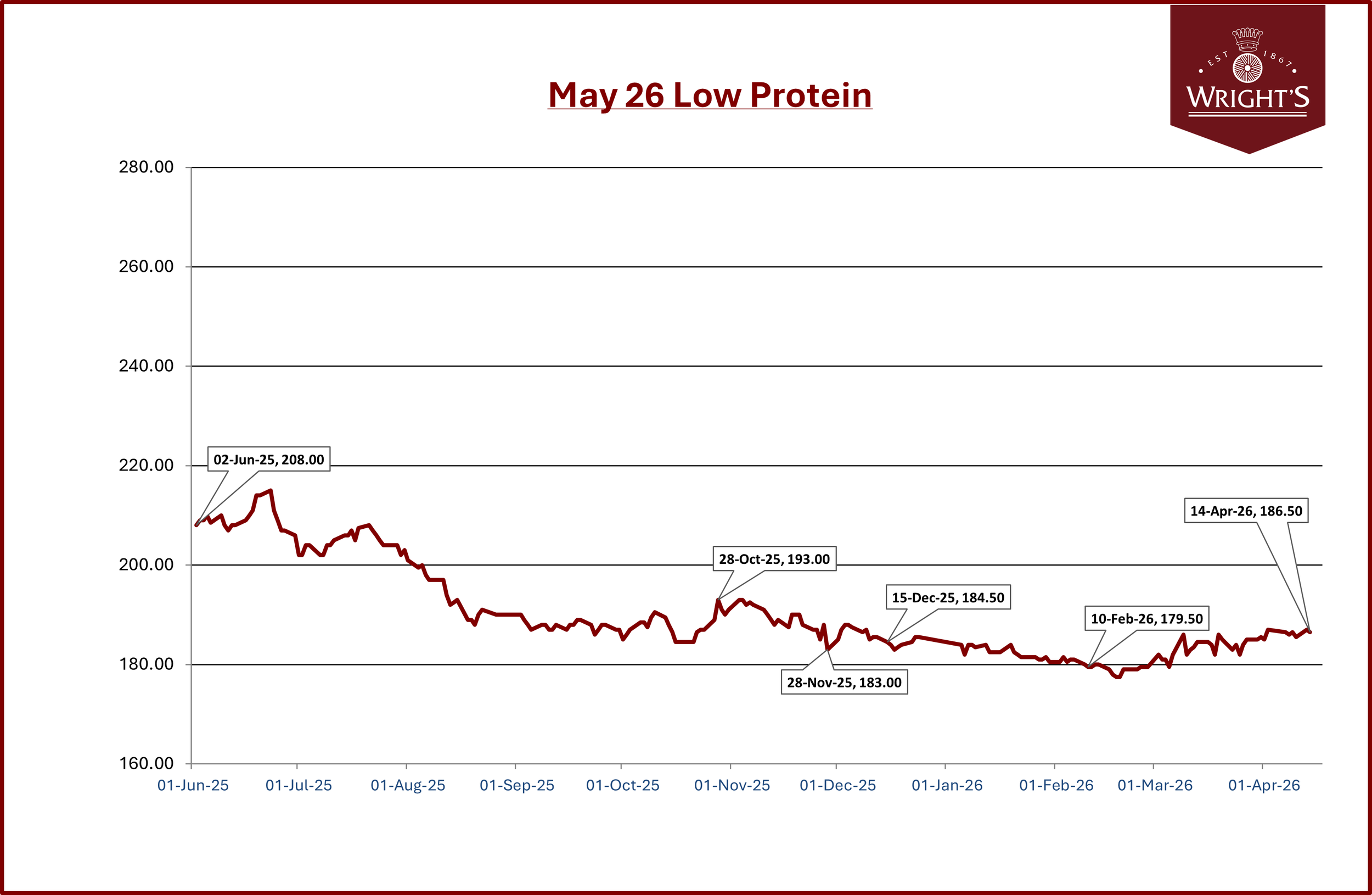

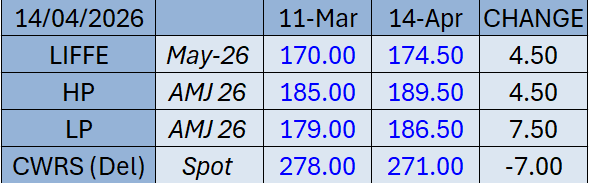

Prices based on May-26 Futures

Market Drivers

Bullish Factors

Energy markets and Geopolitical unrest

Weather challenges for US Wheat

Rising fertiliser prices are lifting production costs

Lower-than-expected USDA forecast for US wheat sowings

Bearish Factors

Comfortable major exporter of wheat stocks

Potential end to the Iran war

Middle East unrest threatens a major importing region

Corn market pressure from the Argentine harvest

Larger-than-expected US corn sowings forecast

Demand destruction for imported grains in the Middle East

Market Report

Global Outlook

Wheat prices recovered ground on Monday with the revival in Middle East tensions, as highlighted particularly by the crude oil market.

Markets continue to closely watch developments around the Strait of Hormuz and the risk of wider regional disruption.

A fragile two-week ceasefire and talks in Islamabad briefly eased concerns throughout last week, but the situation remains highly uncertain, with both sides still exchanging hardline rhetoric and the possibility of renewed escalation hanging over the region.

For grain markets, the main relevance remains the potential impact on energy prices, shipping costs, and broader risk sentiment, all of which can feed through into commodity pricing.

Major exporter supplies for 2025/26 look even more comfortable, with the USDA upgrading its forecasts for exporters’ stocks to their most ample in eight years.

USDA WASDE - The release of the USDA April World Agricultural Supply and Demand Estimates last Thursday put pressure on the market. The report was broadly neutral-to-bearish for grains, with U.S. maize stocks unchanged, at a seven-year high. Further to that, increases to global wheat and maize ending stocks for the 2025/26 marketing year reinforced a comfortable global supply outlook and limited any upside for wheat and maize futures.

Globally, 40% of wheat (winter and spring) is yet to be planted, creating a risk as farmers might reconsider their crops. However, most UK farmers have their fertiliser covered for the coming season.

Winter wheat crops in the US remain in poor condition, with only 35% rated good/excellent, although rains are forecast which has put pressure on Chicago wheat futures. Russian production for harvest 2026 has been revised up from 86.5 million tonnes to 88.7 million tonnes by analysts at Argus, due to a higher planted area and improved yield prospects

In the short term, the ample global stocks and broadly positive new-crop conditions are being overshadowed by geopolitical threats and higher energy prices, with funds having bought large volumes of long positions in recent weeks.

UK Outlook

For the UK Crop the AHDB rates 83% of UK winter wheat as "good to excellent," a significant improvement from 67% last year.

Across the country, winter wheat crops are looking good in the ground and, so far, have benefitted from a generally positive growing season.

The reopening of the bioethanol plant Ensus has added another buyer to the UK market, helping prop up old-crop values. This is especially evident in the North West and Scotland. The government reopened the plant in response to the ongoing conflict in the Middle East and its impact on energy markets.