Wheat Market Update - Harvest is Coming

Market Drivers

Bullish Factors

US wheat harvest forecast at 54-year low

Major exporter stocks decline in 2026/27

Strong biofuel demand

Energy market support

Rising fertiliser prices lift production costs, threaten sowings

China may buy significant US grains

Bearish Factors

Comfortable end-2025/26 major exporter wheat stocks

Potential end to the Iran war?

Rain stabilises European crop

Seasonal pressure from Argentine and Brazilian corn harvests.

Start of northern hemisphere wheat harvest.

Market Report

Executive Summary

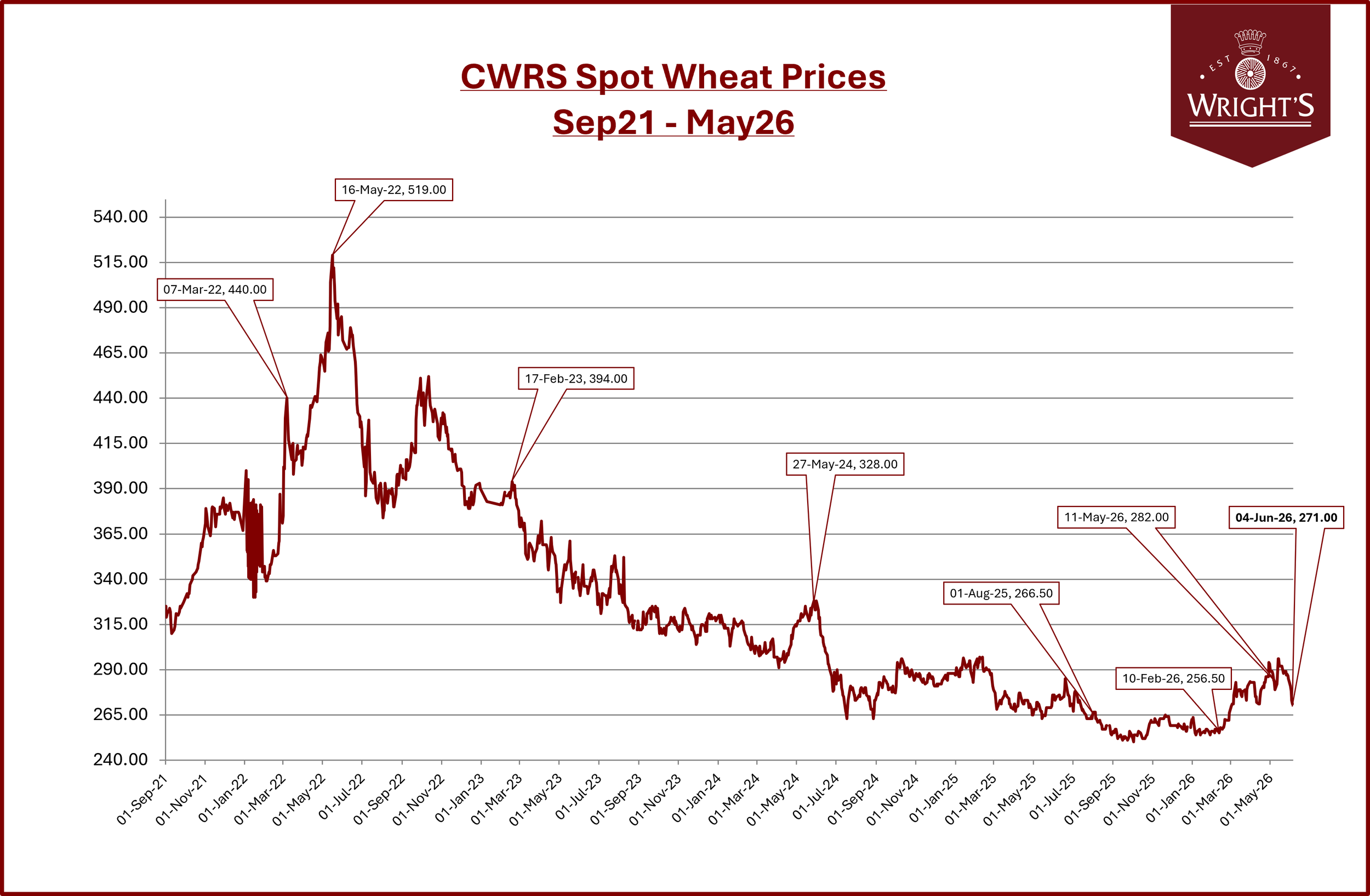

Prices are falling despite bullish fundamentals. Both UK and US wheat futures have retreated sharply from late-May highs, with CBOT wheat now down in 10 consecutive sessions. This disconnect — bearish price action against a backdrop of historically tight US supply — creates both opportunity and uncertainty for buyers.

The May WASDE was striking. The USDA projected US wheat production at 42.5 Mt — the lowest in 53 years, with 70% of the crop area affected by drought. Despite that, global supplies remain large enough, thanks largely to Russia, to keep a lid on prices for now.

The next major price event is 11 June (USDA WASDE). Early US harvest data could push prices in either direction. Buyers with uncovered positions should be aware that the current window of softer prices may be short-lived.

UK has been seeming some good rains - Although

Global Outlook

The big story of the past month has been a tug-of-war between genuinely alarming US crop data and the market's reluctance to sustain a rally. On 12 May, the USDA published its first detailed forecast for the 2026/27 US harvest. It made for sobering reading: total US wheat production is expected at 42.5 Mt (1.561 billion bushels) — the smallest crop in 53 years and 11.5 Mt below last season. Hard Red Winter wheat, the dominant class used in bread flour, has been severely hit by drought across the Great Plains, with 32% of the planted area expected to be abandoned — up from 25% last year.

Since then, prices have fallen for 10 straight sessions. CBOT Jul-26 was trading at 585.25 USc/bu ($215/t) on the morning of 4 June — down nearly 15% from the May peak. Two factors explain the reversal. First, improved rainfall across Europe in late May eased fears about the EU crop. The EU's MARS crop monitoring service estimates EU soft wheat yield at 6.01 t/ha — 5% below last year but still 2% above the five-year average — suggesting a smaller crop but not alarming.

Second, Russia remains a dominant force. SovEcon estimates the 2026 Russian harvest at 90.3 Mt, and Russia's Agriculture Minister has indicated exports of around 50 Mt this season — a volume large enough to keep competitive pressure on all origins. Russian FOB export prices held at $243–$245/t through late May, with an estimated 3.0–3.4 Mt shipped in May alone.

As of last week, harvest had reached 14% completion in Texas, and 7% in Oklahoma, with some early cuts in Kansas, the next Plains state north, also reported.

The 11 June WASDE is the next scheduled catalyst. US harvest has begun in the southern Plains, and early yield data will either validate or challenge the USDA's bearish production forecast. A further deterioration in US crop conditions could rapidly reverse the current downtrend.

Harvest pressure is notable this time of year. Strong harvests in many importing countries look likely to keep a lid on prices, notably in the EU.

UK Outlook

It was for a while looking a little hairy with the general lack of rain around the UK, this coupled with some extreme heat made for concerning news. However, we have since seen some good rains with more forecast. It has been observed that, due to this heat, some areas have seen crops progress through growth stages quickly, with many now predicting an early harvest. Current estimates of crop size are closing in on 13 million tonnes, which would be a good uplift from last season. However, the quality picture is not yet entirely clear, and it's possible we have seen some yield loss as a result of the very hot weather.

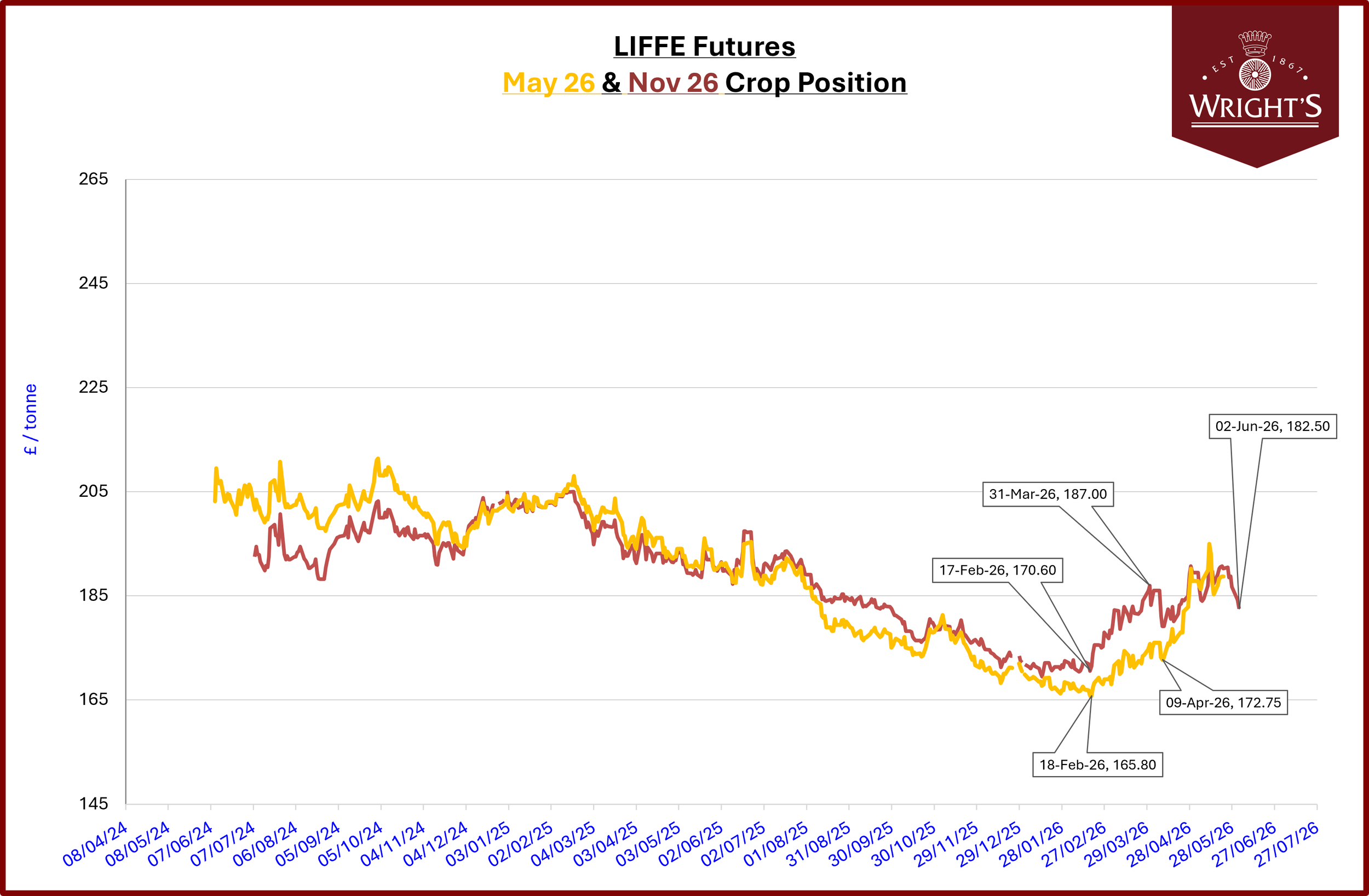

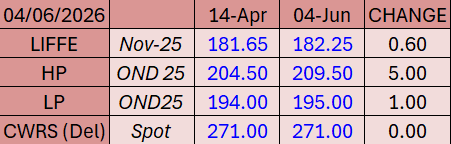

ICE LIFFE Nov-26 feed wheat closed at £186.75/t on 30 May and has continued to ease this week, tracking the global selloff. MATIF Dec-26 milling wheat — the key reference for import parity — was at €215.00/t on 4 June, down from €220.75/t at the end of May.

Old crop prices in the UK remain surprisingly strong, but many buyers are close to being full for June and are holding off further old crop purchases in the expectation of an early start to harvest 2026.

The AHDB have revised their S&D figures to show a carryout from harvest 2025 to 2026 of 1.9 million tonnes, lower than previous estimates. Although East Anglia and the northern home counties remain dry, much of the country has seen good rains in the past few weeks and is forecast to receive more in the next 7 to 10 days.