Wheat Market Update - 20th June 2025

Please note the dash is now based off of the Nov-25 Futures

I. Executive Summary

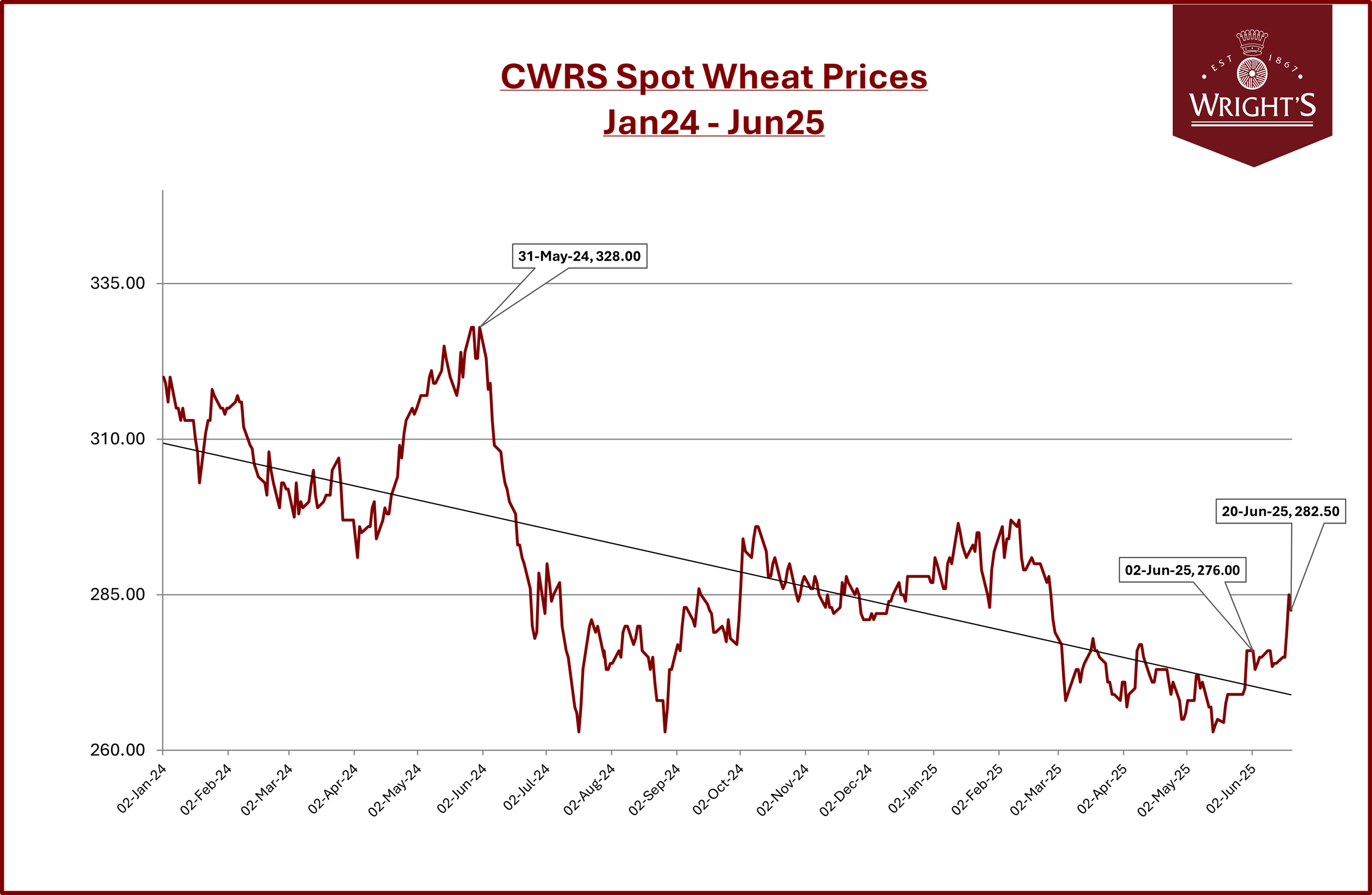

The wheat market is currently navigating a landscape characterised by reasonable volatility, influenced by global supply dynamics, ongoing geopolitical tensions (Israel and Iran), and weather and demand pressures in the UK. Prices have seen an initial rally of nearly £10 from contract lows around June 11th, reaching £184-185 on the Nov-24 futures. This upward movement has been quickly met by underlying bearish pressure, as evidenced by recent declines in global futures. For instance, MATIF Euronext and CBOT contracts have seen slight dips, and UK feed wheat futures also fluctuated downwards.

This pattern of swift price changes, where initial gains are often reversed, indicates a market that is highly reactive to short-term news, such as geopolitical scares or early weather concerns, but is fundamentally constrained by ample global supplies and persistent speculative short positions.

Globally, the latest USDA WASDE report indicates a slight tightening of wheat ending stocks for 2025/26, falling to 262.76 million metric tons, suggesting a diminishing buffer despite generally ample supplies. Geopolitical events in the Middle East continue to foster a "risk-on" sentiment, impacting crude oil prices and freight rates, which in turn elevate grain transportation costs.

In the UK, A very dry spring in 2025, with March and April experiencing the lowest rainfall since 1974 in some areas, has already reduced yield potential, and June rainfall and temperatures will be crucial for the grain fill period. Within the UK, the wheat area for 2025 shows a recovery, up 6% from last year, although it remains below the five-year average.

A significant domestic challenge is the potential closure of major UK bioethanol plants, Vivergo and Ensus, which poses a dual threat: reduced demand for domestic feed wheat and a critical impact on the national CO2 supply, affecting the broader food and drink industry.

II. Global Focus

The global wheat market continues to exhibit a high degree of volatility, significantly influenced by the substantial presence of managed money funds. These funds control over 50% of the open interest and have maintained profitable short positions for the past three years, a factor that contributes to sharp price movements and allows derivative trading to dictate the overall market direction. While overall global inventories are considered ample, this underlying speculative positioning means that any significant bullish news—such as severe weather events or geopolitical escalations—could trigger rapid short-covering.

Geopolitical tensions, particularly in the Middle East involving Israel and Iran, continue to cast a shadow over global markets. While direct impacts on grain shipping have been limited, the conflict has caused a significant rally in crude oil prices, with Brent crude rising 8% to roughly $75 a barrel following recent escalations. This has led to a sharp increase in oil tanker freight rates, with Very Large Crude Carrier (VLCC) rates from the Middle East to China rising by 40%. This directly translates into higher energy costs across the entire supply chain, from farming operations (fuel for machinery, energy for fertiliser production) to international grain transportation, adding upward pressure to grain prices.

Supply and Demand in Key Producing Regions

United States – Exports are set to be the best in five years, but the crop is a touch smaller and stocks, while trimmed, remain above last season.

European Union – A strong bounce-back harvest (about 15 % bigger than last year) should lift exports by nearly a third. Spain and Romania lead the gains.

Black Sea – Russia, Ukraine and Romania all look set for larger crops. The area can meet extra buying from North Africa, the Middle East and South Asia, where local harvests are weaker.

Elsewhere – Argentina could bring in its second-largest crop on record despite recent floods, and India’s grain bins are far fuller than a year ago.

III. UK Focus

An early harvest is anticipated in the UK, potentially beginning as soon as early August, particularly on lighter lands. However, early harvests do not always correlate with strong yields, and concerns persist regarding overall yield potential due to erratic weather patterns. Lighter lands may see earlier harvests but are expected to struggle with lower yields, while heavier lands, having retained moisture, are anticipated to perform better.

Current weather conditions are beneficial for protein generation in milling wheat, which is a positive for quality.

UK wheat production estimates vary: USDA projects 12.8 million tons, Strategy Grains 12.7 million tons, while some analysts are more optimistic, estimating 13.3–13.4 million tons. This contrasts with 9.5 million tons in 2020 and 11-11.1 million tons last year.

The UK wheat area for harvest 2025 is estimated at 1,623 kilo-hectares (Kha), a 6% increase from last year's four-year low, slightly exceeding initial grower plans due to improved autumn weather.3 However, this remains slightly below the five-year average (2020–2024) of 1,648 Kha

UK Bioethanol Plant Operations

The situation surrounding UK bioethanol plants, Ensus and Vivergo Fuels, has become a domestic concern. Both plants, which use UK-grown wheat to produce bioethanol for E10 petrol, are facing imminent closure threats unless they receive financial support from the government. This vulnerability is primarily attributed to a recent US-UK trade deal that allows 1.4 billion litres of US ethanol to be exported to the UK tariff-free, effectively undercutting domestic production. US manufacturers already benefit from lower crop and energy costs, making it nearly impossible for British producers to compete.

The threatened closure of these plants is not merely a localised issue of reduced wheat demand; it represents a significant supply chain vulnerability for the UK. Vivergo, for example, uses feed-grade wheat from over 12,000 UK farms, meaning its closure would directly remove a significant domestic demand source, potentially depressing feed wheat prices for UK farmers.